Trump's Pivot to Section 122

After the Supreme Court’s ruling last week that the “IEEPA does not authorize the president to impose tariffs,” Trump was left with the decision of what to do next. This decision followed a majority consensus — both Kalshi and Polymarket had been trading at a 65–70% probability of a ruling against the tariffs since December. The justices were vague on the timeline for refunding, punting the ball to the International Trade Court to decide the distribution of reimbursements.

Trump described the justices’ decision as “an unfortunate ruling” in his State of the Union address on Tuesday. After the decision, the effective tariff rate fell to 9.1%.

Trump was left with two decisions post-SCOTUS ruling:

(1) He could use this as a retreat, claim effectiveness of tariffs, and use the Supreme Court ruling as justification for any future negative fallout.

(2) He could impose additional tariffs through use of the Trade Act of 1974, the Trade Expansion Act of 1962, or the Tariff Act of 1930, among others.

He went with the latter option, imposing a 10% ad valorem tax using Section 122 of the Trade Act of 1974. This caused the effective rate to rise to 13.7%, a decrease from the 16% effective rate under IEEPA. Compared to the IEEPA, Section 122 is much more constrained in that it permits a surcharge not exceeding 15%, expires in 150 days, and requires a defensible macroeconomic justification.

This ruling made clear that broad emergency laws like the IEEPA cannot be used by a president to impose tariffs and that Congress has clearly delegated the power to the executive branch in specific tariff statutes. The argument going forward will not be whether a particular statute authorizes the president to impose a tariff, but rather whether the economic condition is present and the justification is valid. This is a narrower argument, one that is a question of economic facts rather than an interpretation of the law.

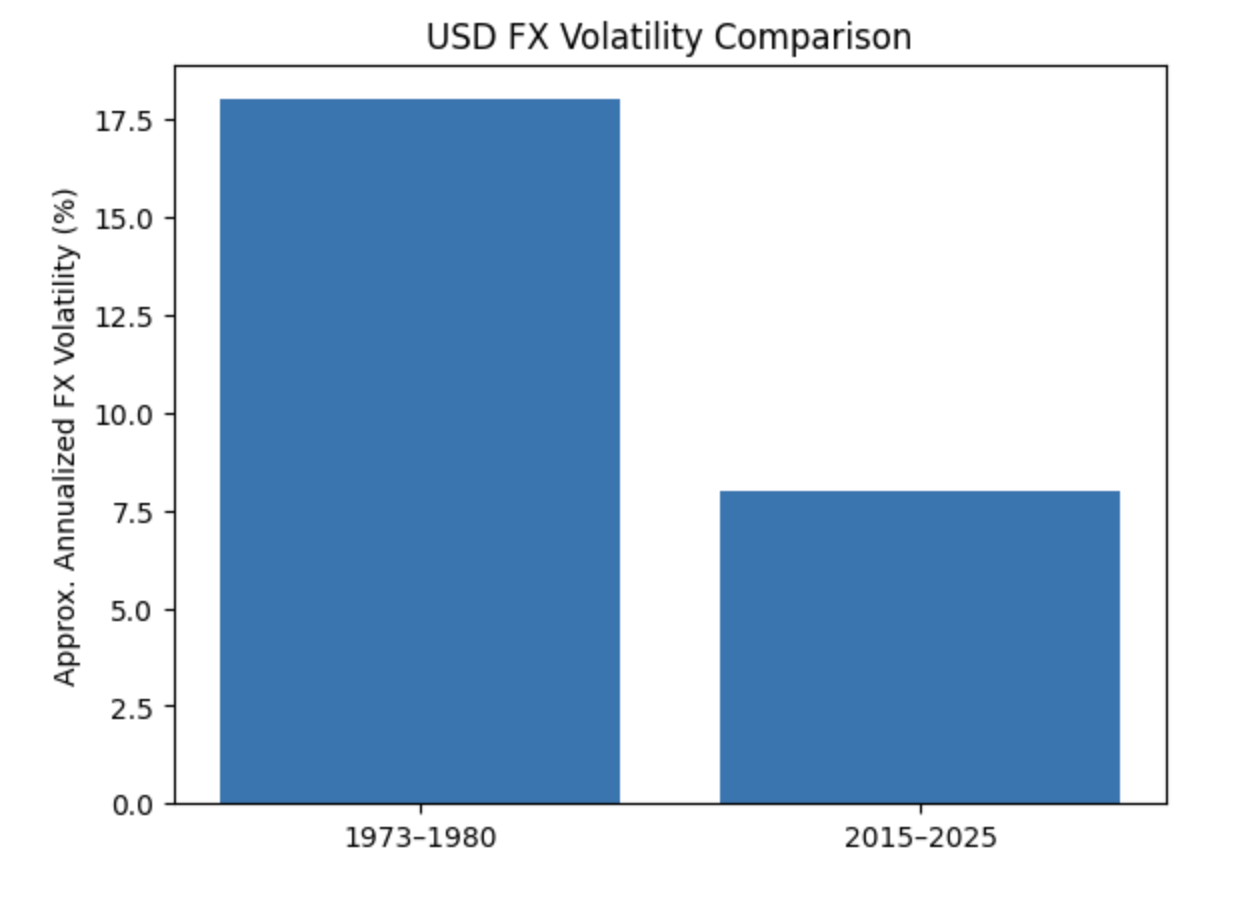

In the case of Section 122, the question is whether we are facing a “fundamental international payments problem.” From the start of the Bretton Woods system in the early 1960s (when the dollar was convertible to gold at $35/ounce), to the Nixon Shock in 1971 (suspension of dollar convertibility and a 10% import surcharge), to the collapse of Bretton Woods in 1973 (a pivot to floating exchange rates), this was a period of major instability in FX rates, rising inflation, and decreasing confidence in U.S. macro policy. This is the backdrop for the creation of Section 122. It was intended to serve the role that the Nixon Shock had in 1971 — a tool to respond to a crisis and force exchange-rate adjustments.

It lays out three reasons for the act to be used:

(1) To deal with large and serious United States balance-of-payments deficits,

(2) To prevent an imminent and significant depreciation of the dollar in foreign exchange markets, or

(3) To cooperate with other countries in correcting an international balance-of-payments disequilibrium.

The administration is going with the deficit defense. In Trump’s proclamation authorizing Section 122, he writes, “I find that a surcharge in the form of ad valorem duties on certain imports is required to deal with the United States’ large and serious balance-of-payments deficit.”

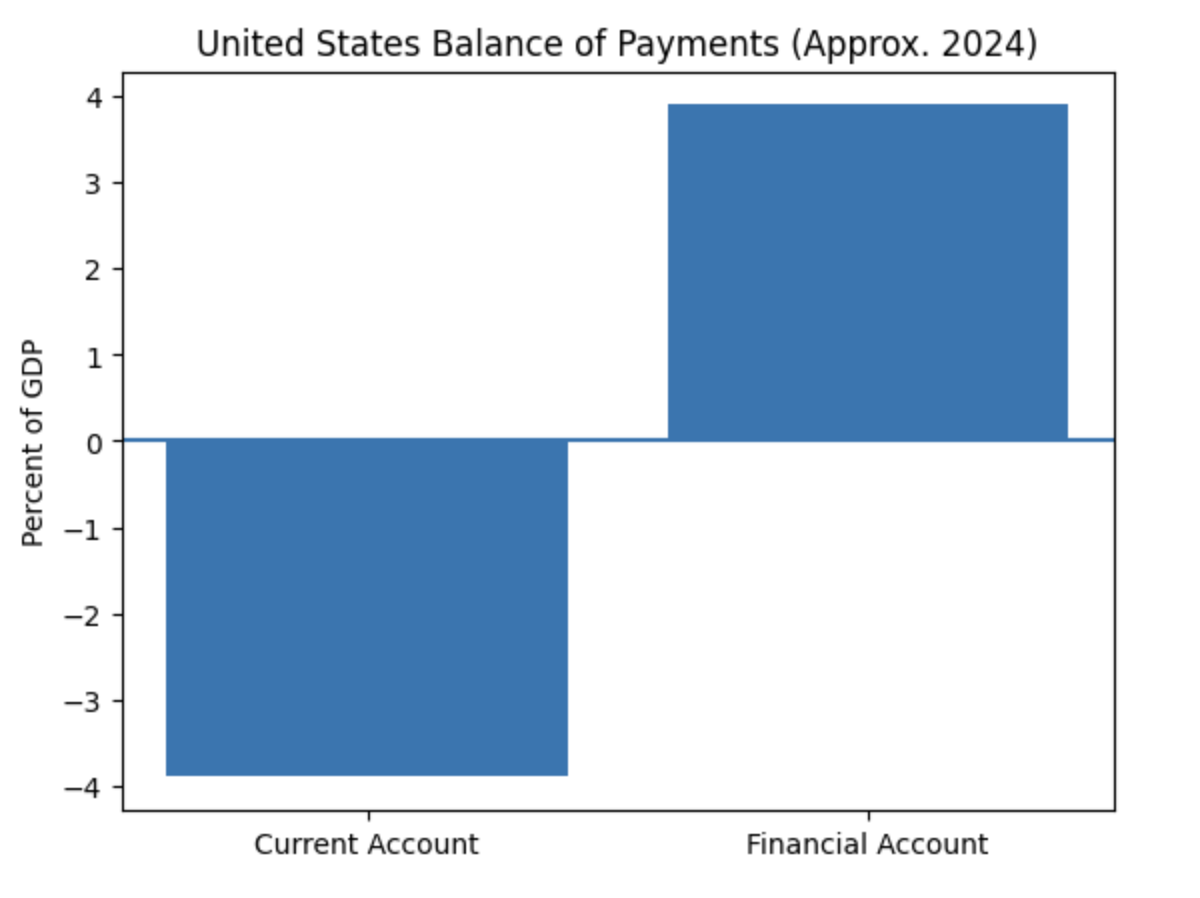

It is important to understand the structure of the balance of payments. It captures transactions between U.S. residents and the rest of the world. Transactions are divided into two separate accounts:

- current account — net flow of money due to U.S. involvement in international trade

- trade balance — value of goods/services the U.S. exports less those it imports

- capital & financial account — net change in ownership of assets/liabilities

- capital transfers — transfer of assets/forgiveness of debts

- direct investment — long-term capital investment (direct influence on operations)

- portfolio investment — purchase of debt/equity (no direct influence on operations)

This is a simplified explanation. Both the current and capital/financial accounts have additional components. Each transaction initiates a double-entry system of debits and credits. Every transaction has both a debit and a credit.

An example of this:

Generac imports $50 million of electric motors from a Chinese manufacturer. Generac pays with cash; this is marked as a cash outflow, a debit to the current account. The Chinese exporter now has $50 million of USD. Those dollars can be used to purchase U.S. goods (export), held in a U.S. bank (inflow), or invested in U.S. financial assets (inflow). For the latter two options, this would create a financial account surplus. Having a financial account surplus means the U.S. is effectively borrowing from abroad or selling domestic assets to foreigners.

In 2024, the trade deficit was $903.5 billion. In 2025, it was $901.5 billion. This implies a financial account surplus of roughly $900 billion over the past two years, or roughly 3% of GDP. Large in absolute terms does not imply distress; as a share of GDP, the deficit remains within historical ranges. A deficit, in and of itself, is not a bad thing.

Nikolai Wenzel, a Senior Fellow at the American Institute for Economic Research, wrote an article for independent.org which I think does a very good job summarizing why a financial account surplus is not a bad thing:

“Just as the U.S. is the biggest economy in the world, it is also the most attractive for foreign investors, and this is for many reasons. The U.S. has a strong tradition of rule of law and protection of property rights. It has deep and liquid financial markets — so deep, in fact, that the U.S. alone has the largest share of the world’s stocks; it accounts for half the value of the world’s stock capitalization. It’s also easier for Americans to buy stocks directly or through mutual funds. Fully 55% of Americans own stock, as opposed to 33% of Britons, 15% of French and Japanese, 14% of Germans and Dutch, 7% of Italians and Chinese, 6% of Indians, and 5% of Belgians. Add to that the dollar’s role as the international currency, and it’s little wonder that almost a trillion dollars’ worth of foreign investment flowed into the country last year.”

What would create an environment for “serious” balance-of-payments problems?

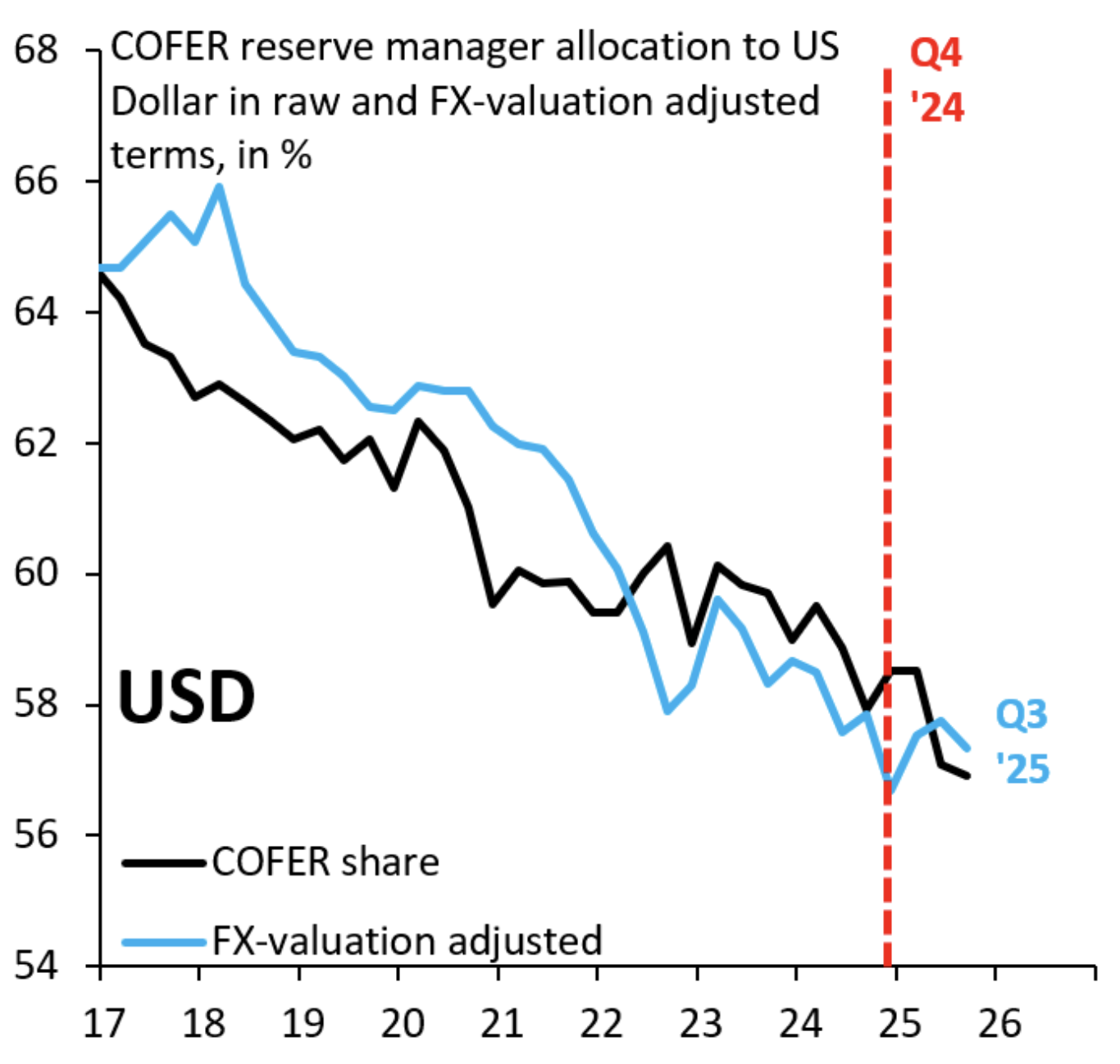

- Sharp depreciation in the dollar — the dollar has fallen 10% since Trump took office, but as Robin Brooks notes, while it will likely continue to fall, this is mostly due to “policy chaos in DC,” and IMF data shows that reserve managers have not reduced allocation to the dollar.

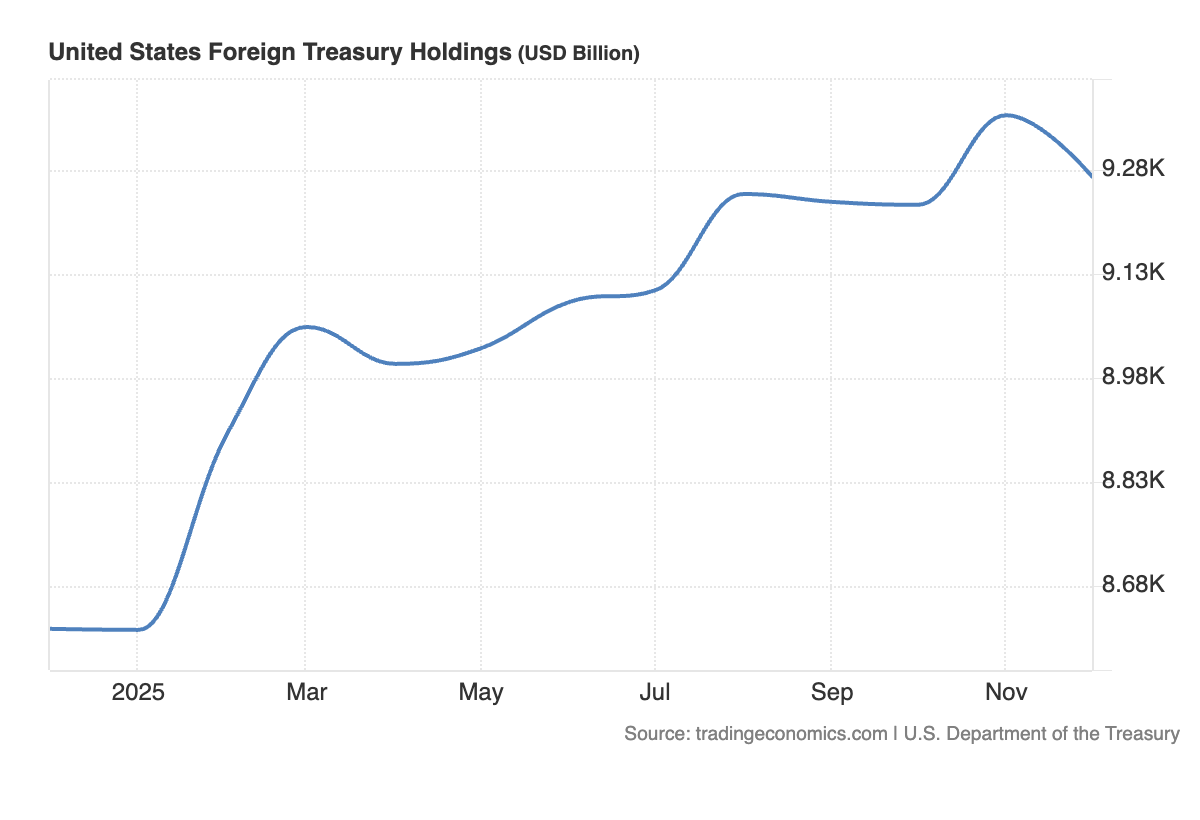

- Persistent capital outflows — this is not the case. Capital inflows reached record highs in late 2025, and major holders continue to maintain large positions despite a broader diversification trend.

- Failure of markets to attract capital — same case as above; we have seen strength in markets.

Our current macro environment shows no evidence of a serious balance-of-payments deficit. Much like the Trump administration’s use of IEEPA prior to the Supreme Court’s ruling, I believe that the current use of Section 122 faces substantial legal vulnerability and appears inconsistent with legislative intent.

Comments