Impact of Iran Oil Shock on Asian Naphtha Markets

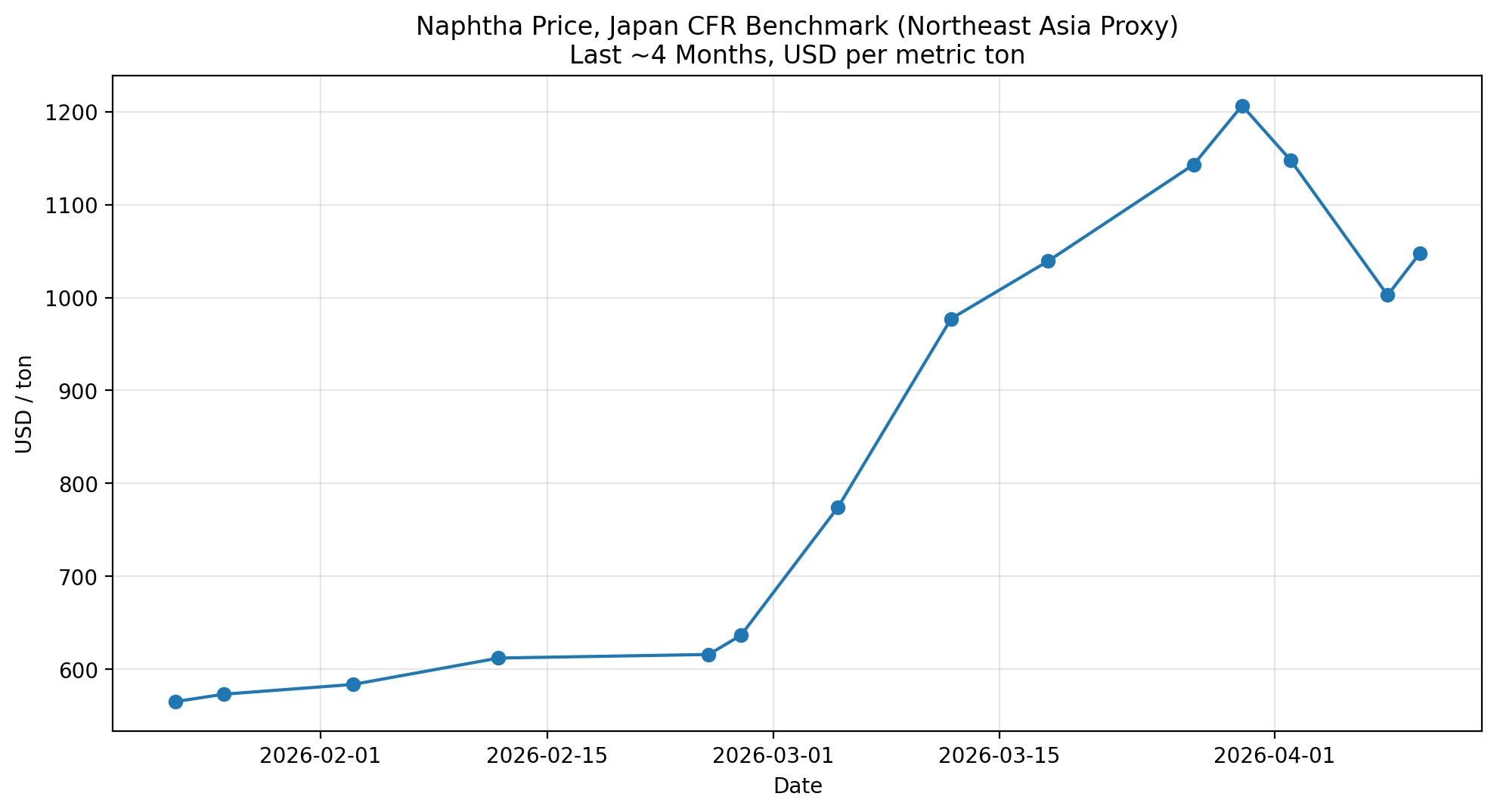

I started writing this article soon after the conflict in Iran began, but never got around to finishing it. Since then, the situation in naphtha markets has only deteriorated. What initially appeared to be a localized disruption has now evolved into a broader petrochemical supply shock. It takes roughly 40 days for a tanker to transport crude or naphtha from the Middle East to Asia. The conflict started 45 days ago, Asia is only now receiving the final shipments of pre-war crude. JPMorgan reported that the last batch of pre-conflict crude arrived in Asia by April 10th. As a result, while the effects of the disruption began soon after the war started, shortages in crude and downstream petroleum products are likely to persist and worsen.

Several weeks ago, the disruption was largely concentrated among naphtha crackers in Japan and Korea, many of which had already declared force majeure as feedstock costs became unsustainable. The impact quickly began moving downstream. Reece Group, a major plumbing supplier in Australia, informed customers that it would be raising the price of PVC pipe and fittings by 28.5% to 36% depending on product type. Since then, the shock has spread much further, with price increases now visible across plastics, chemicals, and consumer goods. Below is a sampling of some of the announced price hikes:

| Company / Entity | Product | Price Increase |

|---|---|---|

| Seven-Eleven (Korea Seven) | Trash bags | +36.8% to +39% |

| Dow Inc. | Polyethylene (resins) | Increased planned hike to +30¢/lb |

| Lanxess | Plasticizers / specialty chemicals | Up to +50% |

| Celanese | Engineered materials / acetyl chain | Double-digit increases (up to ~50%) |

| BASF / Wacker Chemie | Chemicals / plastics | Industry-wide increases up to ~50% |

| Korea Prepac | Polyethylene packaging film | Capacity cuts (20–30%) with price increases |

| Expandable polystyrene (Asia buyers) | Foam / packaging materials | ~+35% |

| Bisleri | Bottled water (plastic bottles) | +11% |

| Ecolab | Industrial / chemical services | +10–14% surcharge |

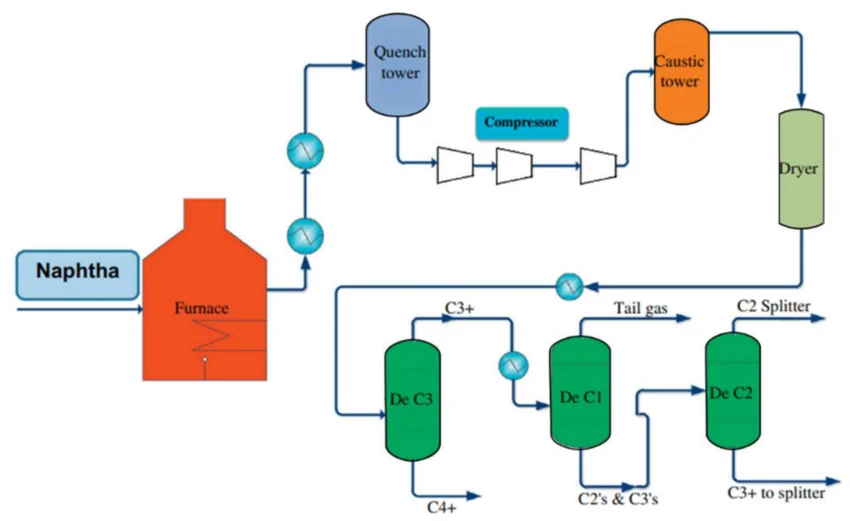

You may have seen naphtha at the hardware store or if you have ever used a MSR white gas camping stove (probably very few people), but may be unfamiliar in the critical role it plays in the production of olefins, the foundation for producing plastics and chemicals. Naphtha, like gasoline, is a light hydrocarbon fuel that is derived from the crude oil refining process. As represented with the diagram below, naphtha is heated in a furnace where the hydrocarbons break apart into smaller pieces. After the cracking process you have a mix of molecules with different numbers of carbons, these are then separated by De C1 (methane - fuel), De C2 (ethylene - flexible cost-efficient plastic), De C3 (propylene - used in polypropylene), C4+ (butadiene - synthetic rubber).

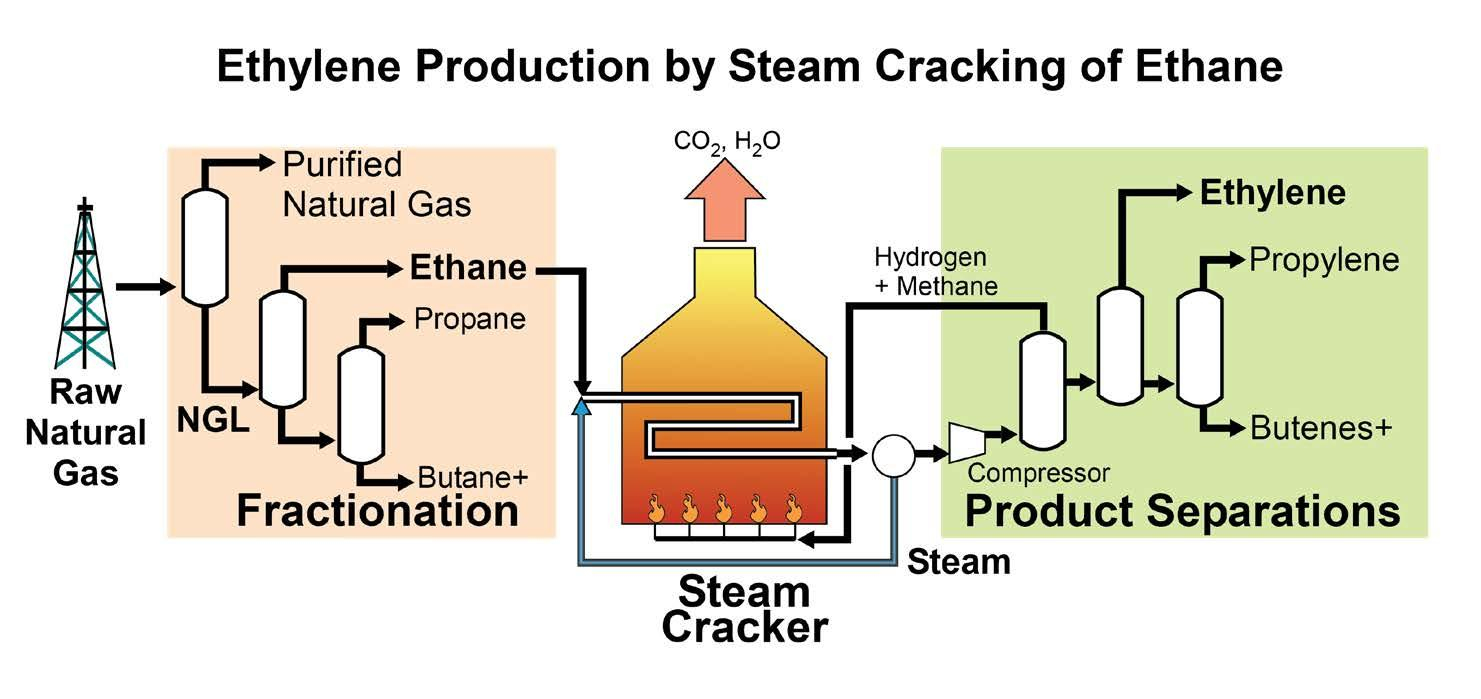

Fully understanding the process is not critical, but the key point is that naphtha produces the full spectrum of petrochemicals in a single system. In contrast, cracking lighter hydrocarbons such as ethane or other NGLs (propane, butane) produces primarily ethylene (roughly 80%) with only minimal amounts of heavier products. For producing ethylene ethane fed crackers are much more efficient, producing 2x the ethylene yield given the same tonnage of feedstock. The diagram below shows the process. Additionally, ethane cracking produces less waste, is more energy efficient, and requires fewer product separation steps. The efficiency of ethane cracking and reliability of NGLs from the Middle East and North America marked a significant threat for naphtha-fed crackers.

This means that while ethane cracking can efficiently replace lost ethylene (C2), it cannot replace the supply of heavier hydrocarbons (C3 and C4), which remain structurally dependent on naphtha. Naphtha-based systems account for roughly one-third of global propylene (C3) supply and the majority of butadiene (C4), and remains a primary source of aromatics.

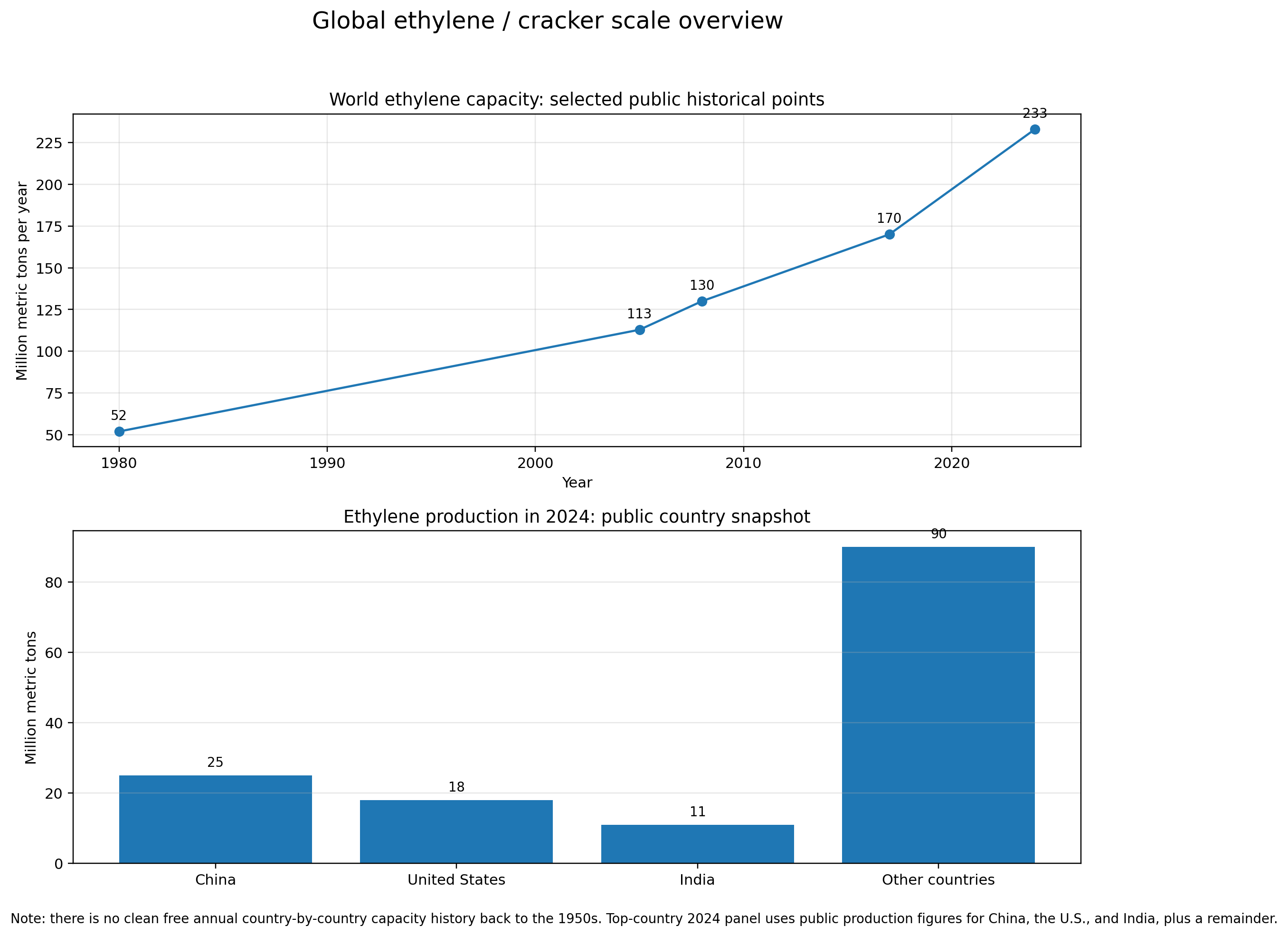

This shock has been particularly acute in Japan. Japan’s first commercial cracker was built in the late 1950s, and from the 1960s through the early 2000s these facilities were highly successful. This success was driven by several structural advantages: inexpensive Middle East oil, tight refinery integration, strong demand from rapidly industrializing Asia, particularly China, and limited global competition. These advantages were reinforced by Japan’s post-war industrial policy, which prioritized the development of integrated petrochemical conglomerates.

Starting around 2010, these advantages began to fade. Ethane-based cracking in the United States and Middle East became structurally more efficient, Japan’s declining domestic oil consumption reduced refinery integration, and China began a massive buildout of domestic petrochemical capacity. At the same time, global competition intensified. According to the IEA, “China is set to add as much production capacity for ethylene and propylene as presently exists in Europe, Japan, and Korea combined” between 2019 and 2024.

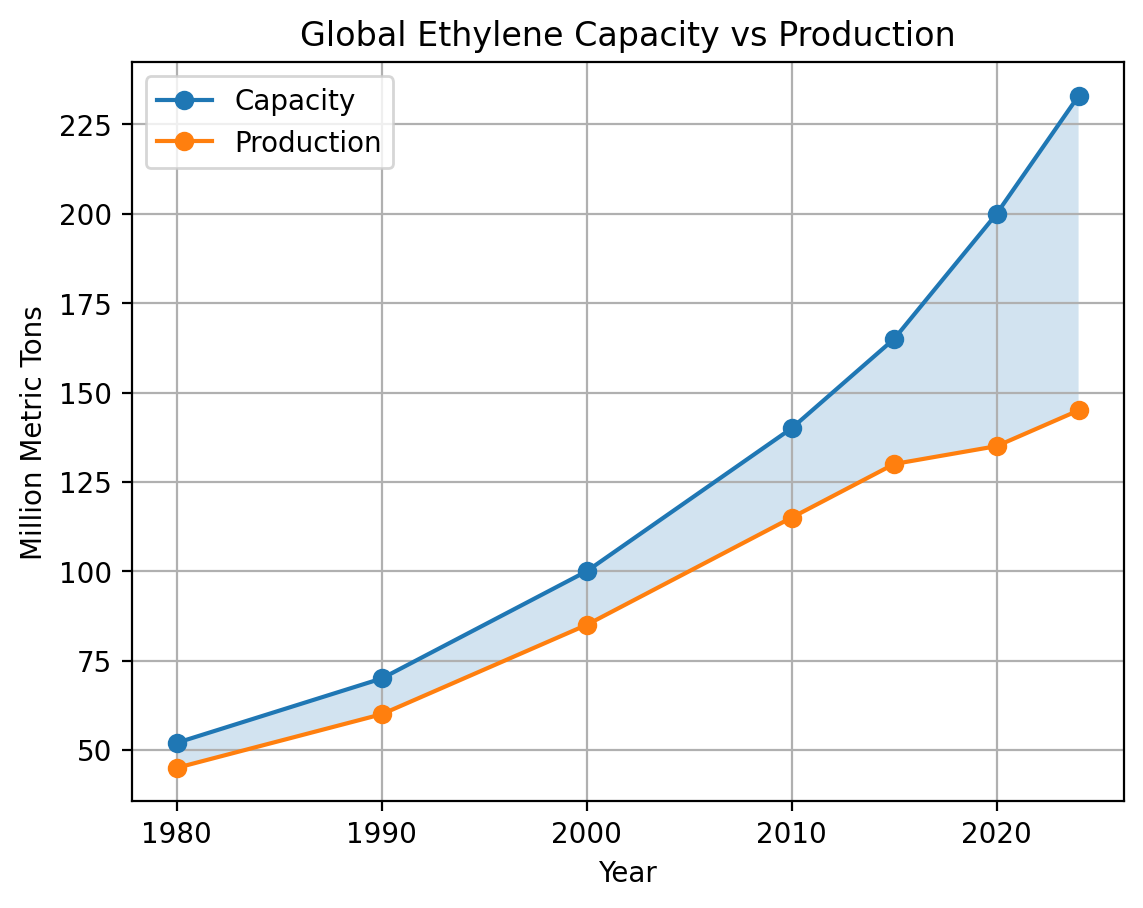

Global capacity utilization is around 65%. This reflects the massive increase in capacity across China, the Middle East, and North America. While plastics demand is still growing, supply has expanded far more quickly, leading to overcapacity.

Unlike North American systems, which are largely based on ethane, Asian crackers rely primarily on naphtha as feedstock, with many facilities unable to meaningfully substitute toward lighter hydrocarbons such as ethane or propane. Japan now produces roughly 6–7 million tons of ethylene annually, a fraction of China’s output and at a significantly higher cost due to smaller crackers and heavy reliance on naphtha. This environment leaves Japanese crackers particularly exposed, as they lack both the cost advantage of ethane-based systems and the scale advantage of newer Chinese facilities.

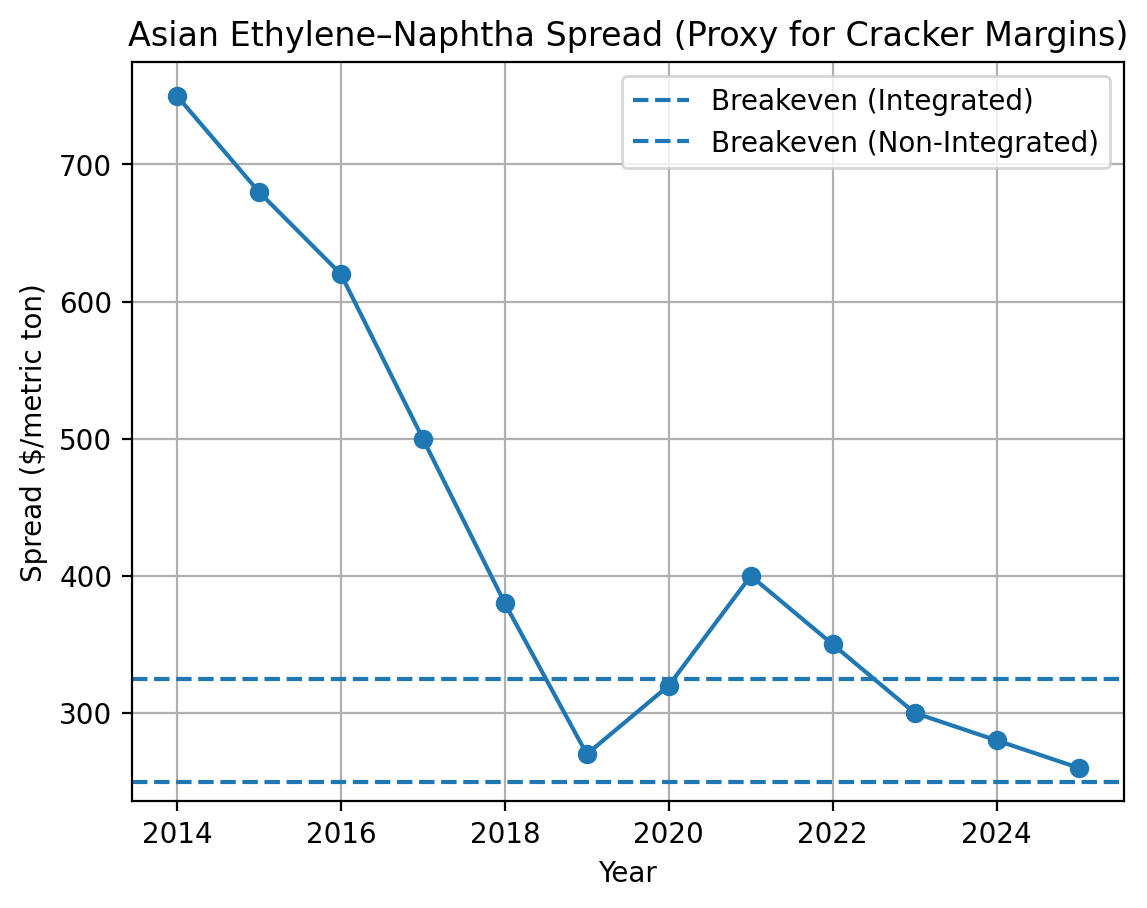

The chart below shows estimated ethylene-naphtha spread based on published figures. The spread is calculated by subtracting Ethylene - Naphtha. Generally reported that ~$250 when cracker is integrated with refinery and just over $300 when non-integrated. As you can see spreads were poor before the conflict started, and have been near break-even since 2019. These spreads were when naphtha was trading at on average in the mid 500s USD/ton (it did reach over 1000 USD/ton during 2022 Russian oil crisis). It is clear that the current surge in naphtha prices will compress these spreads, the closure of several crackers indicates that the spread has dropped well below breakeven.

The implication is that Japanese naphtha crackers are no longer operating as competitive base-load producers, but as marginal suppliers in an oversupplied global market. In periods of stable feedstock costs, these facilities can continue operating near breakeven, supported by their ability to produce a full slate of petrochemicals. However, when feedstock prices rise sharply, as in the current environment, margins quickly turn negative. Cost-advantaged producers in North America and the Middle East continue to operate, while higher-cost naphtha-based systems in Japan and Korea are forced to cut utilization or shut down entirely.

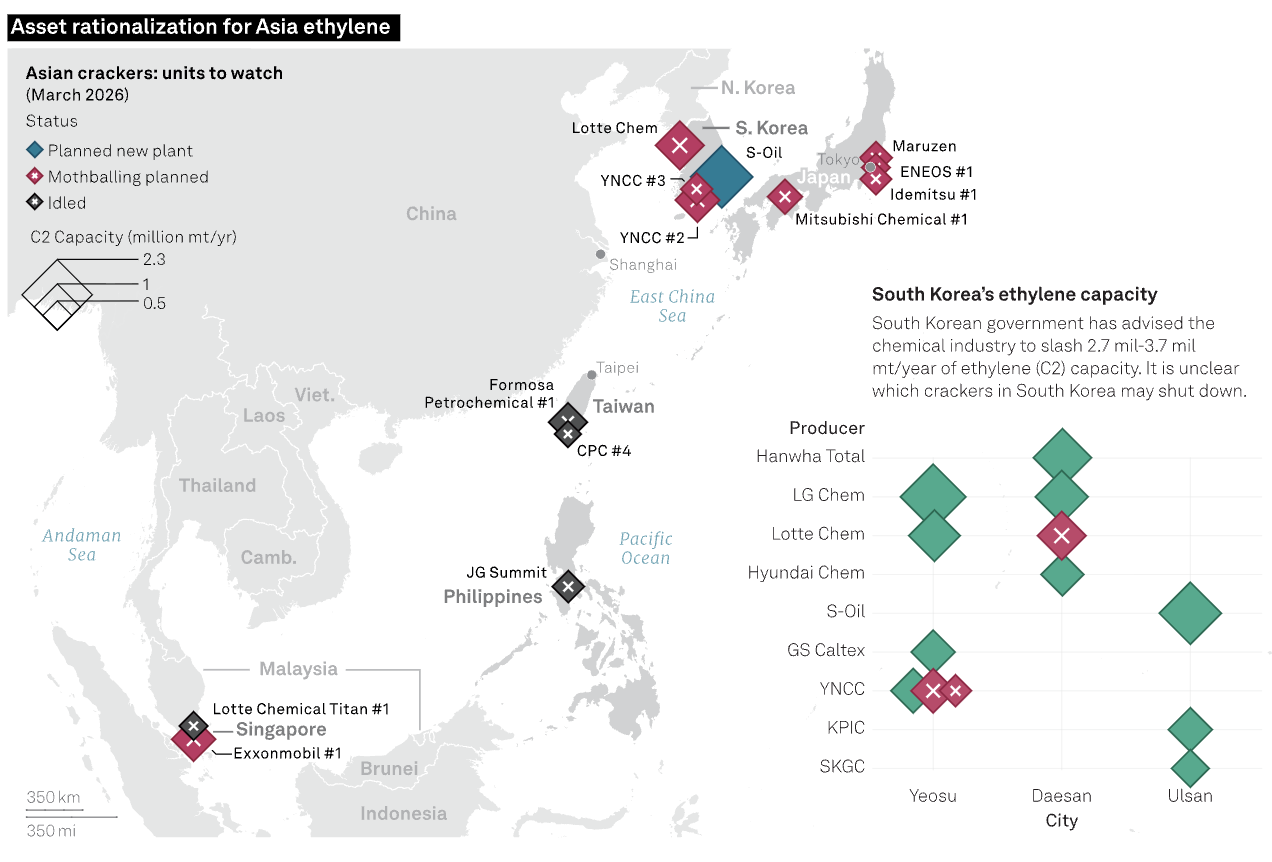

Across South Korea and Japan, several crackers have already announced plans to shut down. In Japan alone, four crackers are expected to close by 2030 (see chart below), removing roughly 1.9 million metric tons of capacity, or about 25–30% of total ethylene production. At the same time, consolidation is accelerating across the industry. In January, Mitsubishi Chemical, Asahi Kasei, and Mitsui Chemicals announced a merger of their naphtha-fed crackers, aiming to reduce costs and significantly cut capacity. In a separate transaction, Japanese firms have also begun consolidating downstream polyolefin businesses in an effort to improve margins and capture cost synergies. These moves reflect a structural shift. Producers are no longer expanding capacity, but are restructuring to remain profitable in a lower-margin, more competitive global market.

This may not mark the final nail in the coffin for Asian naphtha cracking, but it is a clear signal that the fundamental economics that it was built on no longer exist. The current disruption has not created this reality, but it has accelerated the inevitable.

Comments