Housing Affordability: Introduction

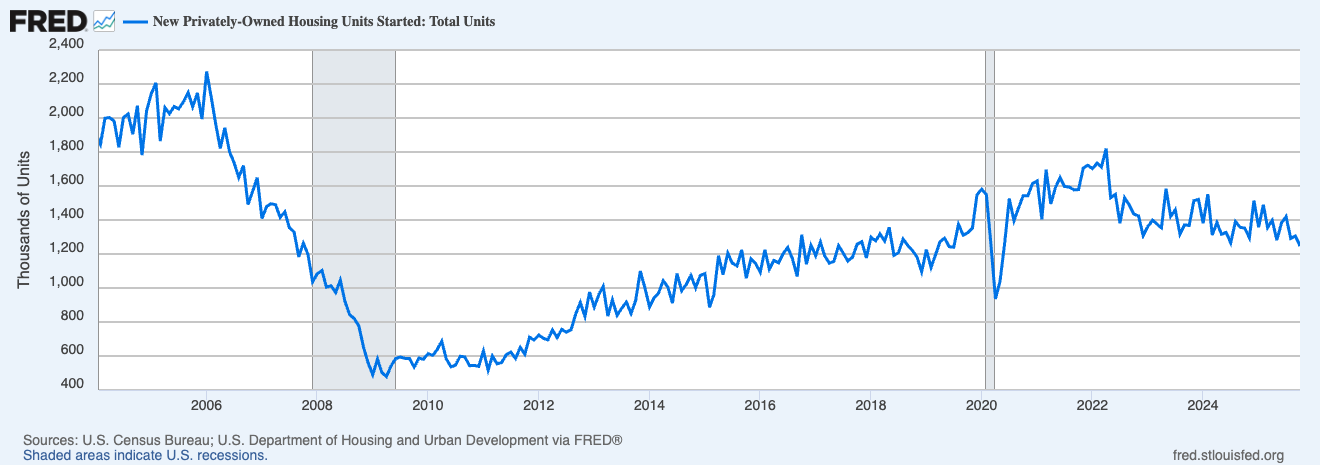

Housing affordability has become one of the defining economic issues of the current political cycle. The United States faces a supply constraint which dates back to a pull-back in lending post-GFC. Years of constrained housing starts, rising regulatory burdens, and labor shortages have casued a decline in long-run elasticity.

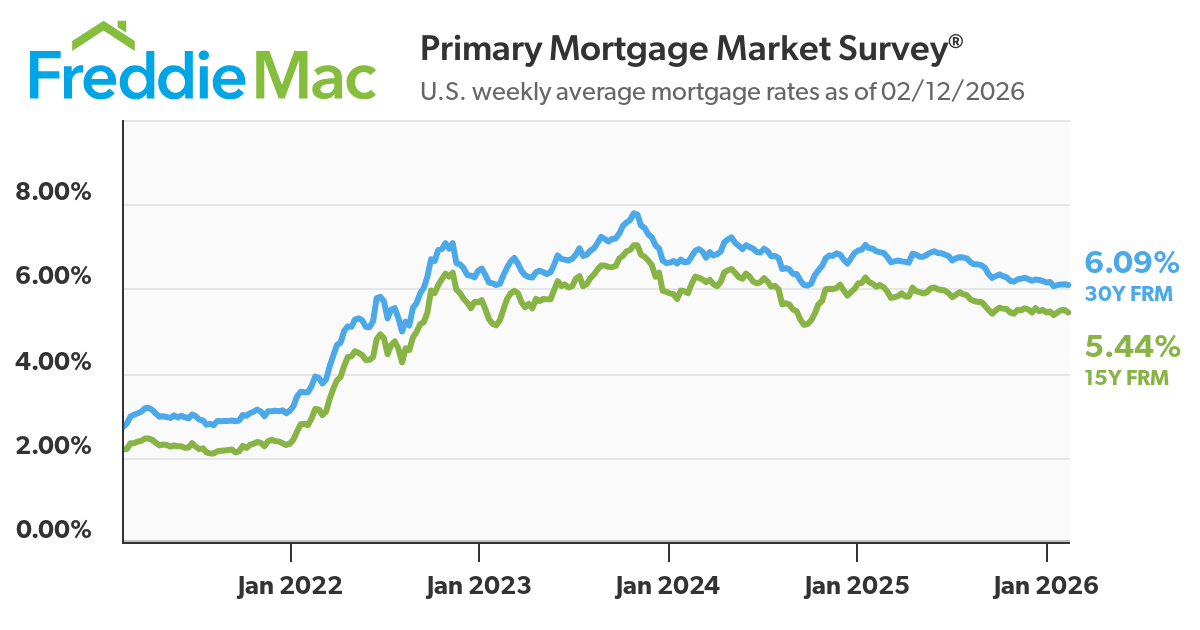

At the same time, today’s affordability pressures are being amplified by elevated mortgage rates. The rapid rise in financing costs has dramatically increased monthly payments, even in markets where home prices have moderated. This rate-driven shock has layered on top of an already tight supply environment, making affordability conditions appear even more severe.

With the midterm elections approaching, policymakers have responded with a series of initiatives that predominantly stimulate housing demand. While demand-side stimulus can be effective in certain environments, history suggests that in supply-constrained markets such measures risk pushing prices higher rather than increasing housing availability. Housing presents an interesting balance. Many homeowners have upwards of 40% of their net worth tied up in home equity, so any decline in housing prices would significantly impact a large portion of home-owning consumers. Trump has said he “wants to drive house prices up,” yet at the same time is pushing to make homes more affordable for first-time buyers through lower interest rates.

Last Monday, the Housing for the 21st Century Act (H21 Act) was approved by the House. Unlike many recent proposals, this bill has the potential to address underlying supply-side constraints, particularly those related to lending requirements, rather than simply expanding purchasing power.

In subsequent articles, I will examine the risks of demand-side incentives, evaluate whether the H21 Act represents a meaningful step toward improving long-term affordability, and outline my predictions for the performance of homebuilders, mortgage providers, and suppliers in 2026.

Current policy landscape:

| Policy Name | Actor | Incentive |

|---|---|---|

| Fannie/Freddie $200B MBS Purchases | Trump Administration | Demand |

| Executive Order Restricting Institutional Investors | Trump Administration | Demand |

| Higher Conforming Loan Limits (FHFA) | FHFA / Federal Housing Agency | Demand |

| Housing for the 21st Century Act (H.R. 6644) | Congress | Supply |

| American Homeownership Opportunity Act (H.R. 3475) | Congress | Both (Demand + Supply) |

Comments